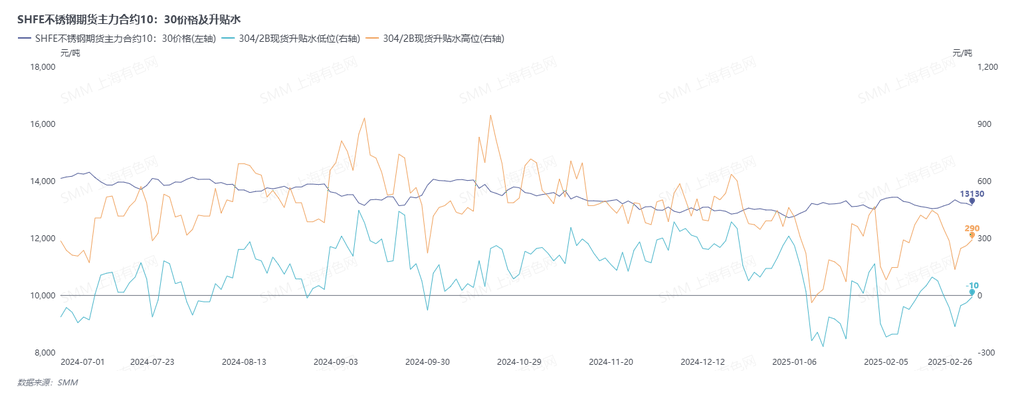

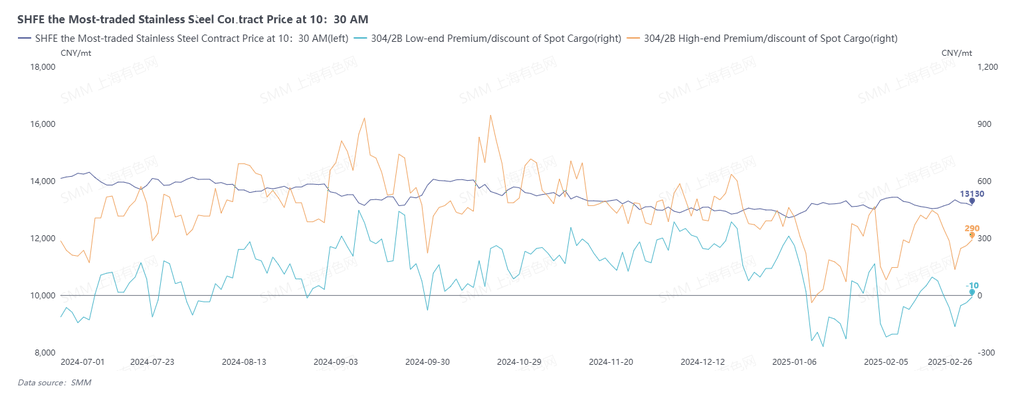

On February 26, stainless steel market prices slightly declined, with mediocre performance in transactions.

Based on the 10:30 price of the SHFE stainless steel most-traded futures contract, the SS2505 contract was quoted at 13,130 yuan/mt. In Wuxi, stainless steel spot premiums ranged from -10 to 290 yuan/mt. Note: spot trimmed-edge price = mill-edge price + 170 yuan/mt.

In the spot market, for 200-series stainless steel, the average price of 201/2B coils in Wuxi was 7,725 yuan/mt, down by 25 yuan/mt from the previous day; the nationwide average price was 7,830 yuan/mt, down by 15 yuan/mt. For 300-series stainless steel, the average mill-edge price of 304/2B coils in Wuxi was 13,100 yuan/mt, down by 50 yuan/mt, while the trimmed-edge average price was 13,600 yuan/mt, down by 50 yuan/mt; the nationwide average price of 304/2B coils was 13,140 yuan/mt, down by 30 yuan/mt. Overall, some stainless steel spot prices declined, and market transactions showed mediocre performance. On one hand, the demand side remained weak, with downstream buyers mostly making just-in-time procurement; on the other hand, although the cost side provided some support, ample market supply limited price increases.

![[SMM Steel] Global crude steel production decreases in Feb y-o-y](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)